Bonds vs. Fixed Deposits: A Comparison of Investment Options

Do you need clarification about whether bonds or fixed deposits (FDs) are better for you? Both are safe investments with fixed returns but have different benefits and risks. FDs are safer because your money is insured up to ₹5 lakh, while bonds, especially from companies, can be riskier. Bonds might not be as easy to sell as FDs, but they can offer more flexibility.

Corporate bonds usually give you higher returns because they come with more risk, while government bonds are safer but offer lower returns. If you don’t like taking risks, FD bonds might be better for you since they offer guaranteed returns. However, it’s essential to consider how much risk you’re comfortable with and your financial goals. A mix of bonds and FD bonds could help you get the best of both worlds: higher returns from bonds and safety from FDs.

First, let’s clarify what bonds and FD bonds are to examine the comparison in more detail. This foundation will help explain how these instruments operate and what to expect from each.

Definitions of Bonds and FD Bonds

Bonds and FD bonds are safe investment options with unique characteristics and advantages.

Bonds

These debt instruments are issued by governments, businesses, or financial institutions to raise money. Bondholders receive regular interest payments and the principal amount when the bond matures. Interest rates vary based on the issuer’s creditworthiness and market conditions. While bond values may fluctuate due to interest rate changes, they are more liquid since they can be traded on the secondary market.

Also Read: Why Fixed Rate Bonds Are Perfect for Conservative Investors in 2024?

FD Bonds

An FD involves depositing a lump sum in a bank or financial institution for a set period at a predetermined interest rate. FDs are known for being safe and predictable and offering guaranteed returns for the investment period. Investors can choose between cumulative or non-cumulative interest payout options. Although early withdrawals from FD bonds may incur penalties, bonds generally offer more liquidity.

Bonds are suitable for investors seeking higher returns and diversification, while FDs appeal to those prioritizing stability and guaranteed returns. These investment options serve different financial purposes.

Claim your financial future with Tap Invest. Sign up to explore our exclusive offerings and see your investments thrive in weeks. Earn attractive high returns of Unlisted Bonds worth 17-18% annualized returns and many other investment options, earning you high returns. Earn with Tap Invest today.

Now that we have the basics of bonds and FD bonds let’s examine who issues them. The issuer type can greatly influence each investment’s risk and return profile.

Issuers of Bonds and FD Bonds

The main difference between FD bonds and bonds as investment options lies in the issuers’ corresponding risk and return profiles.

Bonds

Various entities, including governments, corporations, municipalities, and states, issue bonds. Government bonds are generally considered safer due to their low risk and sovereign guarantee. However, corporate bonds can offer higher return potential but also come with increased credit risk, depending on the issuer’s financial stability.

Also Read: Government Bonds in India: A Complete Guide

FD Bonds

Banks, post offices, and other financial organizations provide FD bonds. As banks are regulated and deposits are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC) up to a certain amount, FDs are considered safe investments.

FD bonds are ideal for risk-averse individuals seeking stability and predictable income, while bonds are better suited for investors looking for higher returns and greater diversification.

Next, we discuss returns, among the most crucial aspects of any investment. Both bonds and FD bonds provide fixed returns, but there can be significant differences in how these returns are generated and taxed.

Returns of Bonds and FD Bonds

Depending on an investor’s financial objectives and risk tolerance, bonds and FD bonds offer different benefits, especially regarding returns.

Benefits

| Bonds | FD Bonds |

| Bonds yield returns through regular coupon payments and price fluctuations in the secondary market. | FD bonds provide steady, guaranteed returns with a fixed interest rate throughout the deposit period. |

| Total return is calculated using Yield to Maturity (YTM), which includes all financial gains or losses. | Suitable for risk-averse investors seeking assured returns. |

| Returns may surpass those of FDs, depending on market conditions and the bond issuer’s credit ratings. | Returns of FD Bonds might not surpass bonds. |

Also Read: How State-Guaranteed Bonds Offer Safety and Steady Returns for Investors?

Taxes

| Bonds | FD Bonds |

| Taxation on bond returns depends on the holding period. | Tax Deducted at Source (TDS) applies if interest exceeds a certain threshold. |

| Long-term capital gains may be taxed at reduced rates. Government bonds may offer tax-free interest. | Interest earned is taxed according to the investor’s tax slab. |

Investment Period

Bonds may have varying investment periods and can be sold in the secondary market before maturity. Whereas, FD bonds offer flexible investment tenures ranging from 7 days to several years, ideal for short-term investments.

Fixed deposits (FDs) provide a secure return but have a lower rate than bonds, which offer higher potential returns but also involve market risks.

With Tap Invest, you can receive assistance selecting the best course for your financial future. Earn high potential investment returns, with an annualized return of 13–14.5 percent in 30 to 90 days. Follow Tap Invest on Instagram to get the latest insights.

Selecting between bonds and FD bonds requires thorough knowledge of the associated risks. Each carries a unique set of risks, depending on the investment type and issuer.

Risks of Bonds and FD Bonds

Bonds and FD bonds are different types of investments, each carrying their own risks.

Risk Level

| Bonds | FD Bonds |

| Government bonds are safer due to government backing, low default risk, and timely repayment of principal and interest. | FD bonds are considered one of the safest investments. |

| Corporate bonds are riskier as repayment depends on the issuing company’s financial health. They offer higher returns to offset risk. | Deposits are insured by DICGC in India up to ₹5 lakhs, reducing risk. |

| Higher-rated bonds (e.g., AAA) are safer, while lower-rated (junk) bonds carry more risk. | Ideal for risk-averse investors looking for steady returns. |

Also Read: Exploring Government Securities: Low-Risk Investment Options

Interest Rate Sensitivity and Insurance

| Category | Bonds | FD Bonds |

| Interest Rate Sensitivity | Bonds are sensitive to interest rate changes. When interest rates rise, bond prices typically fall, potentially resulting in losses if sold before maturity. | FD bonds are not subject to interest rate fluctuations once the deposit is made. |

| Insurance | No specific insurance for bonds. | DICGC insurance protects deposits up to ₹5 lakhs in the event of bank failure, offering more security. |

While bonds have the potential to yield higher returns, the risk associated with them varies based on the issuer. Considering the DICGC insurance coverage, FD bonds are a much safer option, even though they offer lower returns.

Liquidity is another crucial factor affecting how easily you can access your money. Let’s compare the liquidity options offered by bonds and FD bonds to determine which provides more flexibility.

Liquidity of Bonds and FD Bonds

There are critical distinctions between bonds and FD bonds in terms of liquidity that can affect your investment choices.

Bonds

Since bonds can be traded on the secondary market, they offer more liquidity. This means that, depending on market conditions and price fluctuations, you may be able to sell your bonds before they mature and realize gains or losses. As a result, bonds are a more flexible investment option, giving investors better access to their money.

Also Read: Understanding Money Market Instruments: Types, Features, and Benefits

FD Bonds

Conversely, FDs have terms that require you to commit your money for a set period. While they do allow for early withdrawals, there are usually penalties associated with them. Consequently, FDs are a more restrictive investment option because you may incur financial penalties if you need to access your money early.

If liquidity is your top priority, bonds may be the better choice due to their ease of trading despite the inherent risks associated with the market. On the other hand, if safety and predictability are your main concerns, FDs may be the better option, even with their limited liquidity.

We at Tap Invest recognize how crucial liquidity is to your financial choices. Free yourself from the limitations of restricted liquidity by registering with Tap Invest now and learning how our customized solutions can help you effortlessly by watching Tap Invest’s videos on YouTube.

Let’s examine the function of credit ratings in bonds to assess risk even further. While FD bonds aren’t usually rated, some corporate and NBFC FD bonds might offer a credit rating to indicate their safety.

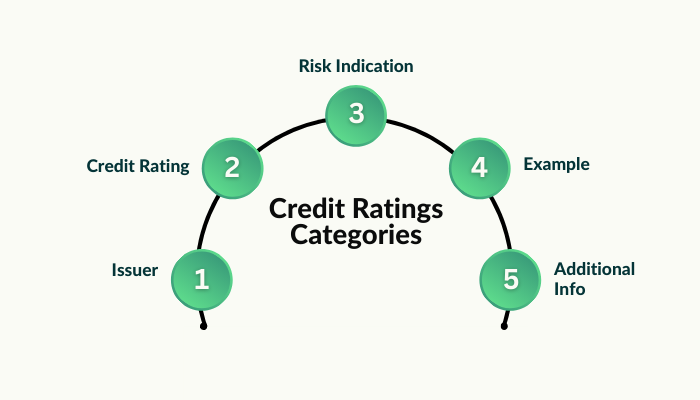

Credit Ratings of Bonds and FD Bonds

Bonds and FD bonds differ primarily in their credit ratings and how they represent the issuer’s creditworthiness.

| Category | Bonds | FD Bonds |

| Issuer | Governments, Corporations, Financial Institutions | Post Offices, Banks, NBFCs, Corporations |

| Credit Rating | Rated by credit agencies (AAA to D) based on credit quality. | Typically unrated, but some corporate and NBFC FDs may be rated. |

| Risk Indication | Higher ratings (AAA) suggest lower risk, while lower ratings (e.g., D) indicate higher risk of default. | Investors rely on the reputation of the issuing institution; ratings are less common but may exist for certain corporate or NBFC FDs. |

| Example | Corporate bonds often have lower ratings than government bonds due to varying risk levels. | Corporate and NBFC FDs may receive ratings, but most FDs are assessed based on the issuer’s reputation. |

| Additional Info | Bond ratings help investors assess the issuer’s ability to repay debts. | Investors in FD bonds often consider the standing of the issuing bank or institution rather than credit ratings alone. |

FD bonds often depend on the financial institution’s reliability, whereas bonds offer comprehensive credit ratings that help investors evaluate risk. Depending on the investor’s risk tolerance and security requirements, this distinction can significantly impact their investment decisions.

Also Read: Investing in AAA Bonds in India: Guide, Rates, and How to Invest

Conclusion

When deciding between bonds and fixed deposits (FDs), there are a few important things to consider, like how long you want to invest, how quickly you might need to access your money, and how much risk you’re willing to take. Bonds can be riskier, but they usually offer the chance to earn more than FD bonds. In contrast, FD bonds are safer because they guarantee your returns, which is better for people who don’t want to take many risks.

Bonds are generally more flexible because you can sell them on stock exchanges before maturity. This means if you need cash, you can sell your bonds. With FD bonds, you can take out your money early, but you might have to pay a penalty that could lower your earnings. While FD bonds are less flexible, they allow you to choose how often you want to receive interest payments, which can help you manage your money better.

Many savvy investors include both bonds and FD bonds in their portfolios. This balanced approach can help mitigate the risks associated with bonds while still offering the potential for higher returns. By carefully considering your options and diversifying your investments, you can create a strategy that aligns with your financial goals and effectively manages risks.

Meet your financial objectives with Tap Invest. It provides many investment options, including Unlisted Bonds, Asset Leasing, and more. We offer choices that cater to your needs if you favor the higher potential returns of Unlisted Bonds and many other options. With Tap Invest, get started on your path now and watch your money grow.