Differences and Comparison between Bonds and NCDs

Have you ever wondered about the fundamental differences between bonds and non-convertible debentures (NCDs) when investing? Although both are necessary for financing, bonds have distinct features that can significantly influence your choices.

Another critical distinction is liquidity; bonds tend to be more liquid than NCDs, which can be more challenging to sell due to their smaller market size and corporate backing. Furthermore, bondholders receive payment before NCD holders during a company’s liquidation, making bonds a safer choice during tough times.

Although both instruments have the potential to yield fixed returns, bonds are issued by governments. They are safer than NCDs issued by corporations and may entail greater risk and higher potential returns. By being aware of these subtleties, investors can choose the best instrument based on risk tolerance and investing objectives.

Before exploring the intricacies of investment options, it’s crucial to grasp the fundamentals before going into NCD vs. bonds. Let’s start by learning what bonds are and how they function in fixed-income securities.

What are Bonds?

Fixed-income securities, called bonds, are offered mainly by corporations, governments, and financial institutions to raise money. They pledge to reimburse investors’ principal at maturity and pay them a predetermined interest amount at regular intervals. To comprehend the distinctions between NCD vs. bonds, keep in mind these critical points:

Issuers

Large businesses and the government generally issue bonds. Because of their government backing, bonds are often considered safer investments.

Security and Repayment at Maturity

These are less hazardous because the issuer’s creditworthiness backs them. During liquidation procedures, bondholders usually have a more extraordinary claim.

Conditions for Issuing

Both bonds and NCDs share characteristics such as a coupon rate (interest rate paid), face value (amount returned at maturity), and maturity date (when the principal is repaid). However, the higher coupon rates on NCDs might draw in investors.

Applications of Funds Raised

Bonds frequently raise money for infrastructure development, public projects, and business expansions. They also usually provide funding for long-term initiatives.

Also Read: Difference Between Zero Coupon and Deep Discount Bonds: Definition, Risks and Advantages

Interest Rates and Orders in the Liquidation Process

Bonds are considered a safer investment because, in most cases, bondholders are ranked higher in the repayment hierarchy during liquidation. Bondholders receive their repayments ahead of NCD holders, particularly in the case of unsecured NCDs.

Horizon of Investment Depending on Issuer Terms

These funds frequently possess extended investment durations, spanning several years to multiple decades.

Bonds and NCDs are both debt instruments. The differences between NCDs and bonds in terms of issuers, security, issuance terms, and intended use of funds affect their risk profiles and investor appeal.

While bonds offer a stable source of income, NCDs present different opportunities for investors. Let’s examine NCDs and how they differ from traditional bonds.

What are Non-Convertible Debentures (NCDs)?

Non-convertible debentures (NCDs) are debt instruments mainly issued by corporations that cannot be converted into equity shares. Like bonds, NCDs provide fixed returns over a predetermined time period.

Standards for Secured vs. Unsecured NCDs

Based on the support they provide to investors, NCDs can be divided into two categories: secured and unsecured.

Secured NCDs

These provide investors with extra security because they are backed by specific assets of the issuer. Secured NCD holders have a claim to the underlying assets in the case of default.

Unsecured NCDs

These lack collateral, which increases their risk. Investors depend solely on the creditworthiness of the issuer to repay their investments. Because secured NCDs offer lower interest rates than unsecured ones, reflecting the lower risk, investors should be aware of this distinction.

Credit Ratings for the Issuer’s Financial Stability

An essential component of evaluating the financial standing of bond and NCD issuers is credit ratings. A higher credit rating denotes a lower default risk, which can attract investors.

For Issuers

A high credit rating serves as a reliable indicator of creditworthiness to investors and can reduce borrowing costs. A low rating, on the other hand, may result in higher interest rates and more challenges when raising capital.

For Investors

Credit ratings offer a quick evaluation of the risk associated with purchasing a specific bond or NCD. To minimize potential losses, investors frequently consider these ratings before making decisions.

Also Read: Understanding Market Linked Debentures: An Investor’s Guide

Function of Credit Rating Organizations (CRISIL, CARE, ICRA)

Credit rating organizations that assess issuer creditworthiness, like CRISIL, CARE, and ICRA, are essential to the bond and NCD markets. These organizations provide thorough credit ratings and insights into the financial stability of different entities, enabling investors to make more informed decisions.

CARE

This organization comprehensively analyzes corporate financial performance and focuses on rating debt instruments.

ICRA

A division of Moody’s Investors Service, ICRA assesses Indian companies’ credit risk and assigns ratings based on the probability of default. By ensuring that investors are aware of the risks involved with their investments, these organizations contribute to preserving transparency in the financial markets.

Although bonds and NCDs are dependable sources of fixed income, their structural distinctions—such as secured versus unsecured status and the implications of credit ratings—underline the importance of careful due diligence and risk assessment before making an investment.

Are you seeking stable returns and a secure investment? At Tap Invest, risk and reward go hand in hand. With our professional advice, we assist you in making wise decisions based on your fixed income. Invest with Tap Invest today.

Now that we’ve covered the basics of NCDs, we must explore why investors might choose to invest in NCDs vs. bonds. Here’s what makes NCDs appealing to certain types of investors.

Investment in NCDs

Learn about the issuer’s risk profile to align your investments. Knowing these factors, you can maximize your investment returns and strategically navigate the NCD market.

Fixed Tenure

NCDs are defined by their fixed tenure and consistent income. Typically, NCDs have maturities ranging from one to ten years.

Periodic Interest Payments

Interest can be paid to investors at predetermined intervals, such as monthly, quarterly, semi-annual, or annual. NCDs are an appealing option for those looking for regular returns because of their steady income stream. Like traditional bonds, they offer investors a consistent income with fixed tenures and regular interest payments.

To Increase Liquidity, One Can List on Stock Exchanges

Unlike traditional bonds, most NCDs are more liquid because they are listed on stock exchanges.

Market Trading

Listed NCDs enable investors to liquidate their holdings before maturity by allowing them to be bought and sold in the secondary market. This critical feature allows investors to access their money before the NCD matures. Certain bonds may not always have this liquidity, mainly if they are not frequently traded on the market, which can impact their resale value.

Also Read: Understanding Redeemable Debentures: Features, Advantages, Disadvantages and Methods of Redemption

Investing Techniques

Investors can purchase NCDs in several different ways. Public offerings are a common way for businesses to issue NCDs, allowing investors to subscribe directly during the issue period. This procedure usually involves a thorough prospectus that describes the conditions, risks, and potential rewards of the NCD.

Secondary Market

NCDs may be traded in the secondary market after being issued. This promotes price discovery based on market supply and demand, allowing investors to purchase or sell NCDs through stock exchanges. Investors can select their preferred method according to their investment strategy and the state of the market, due to the flexibility provided by this dual approach.

Assessing the Risk Profile of the Issuer Before Investing

Before purchasing NCDs, investors must assess the risk profile of the issuer.

Credit Ratings

Credit ratings from organizations such as CRISIL, CARE, and ICRA are essential for investors because they provide information about an issuer’s financial standing and default risk. A higher rating denotes reduced default risk, whereas a lower rating indicates higher risk.

Financial Health

Investors can gauge an issuer’s stability by evaluating its financial statements, which include information on revenue, profit margins, and debt levels. Analyzing factors such as industry position, business model, and economic conditions enhances comprehensive risk assessment.

Fixed tenures, regular interest payments, and increased liquidity through stock exchange listings are just a few of the unique advantages of investing in NCDs. However, before making a financial commitment, investors must carefully assess the issuer’s risk profile.

With a solid outlook of NCD vs. bonds, it’s time to delve into the key differences between the two, which can significantly impact investment strategies.

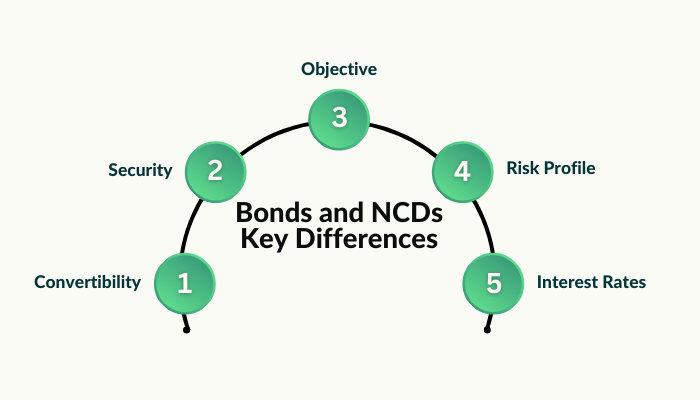

Key Differences between Bonds and NCDs

Investors hoping to steer the fixed-income market successfully must grasp the primary distinctions in NCD vs. bonds. The differences are as follows:

| Feature | NCDs (Non-Convertible Debentures) | Bonds |

| Convertibility | NCDs are not convertible into equity shares of the issuing company. They are fixed-return instruments. | Certain bonds, especially convertible ones, allow investors to exchange bonds for equity shares at a predetermined price. |

| Security | NCDs are usually secured by specific assets of the issuer, providing a safety net in case of default. | Bonds may or may not be secured. Some have collateral, while others depend on the issuer’s creditworthiness. |

| Objective | NCDs are primarily issued to raise money for specific business initiatives or operational needs. | Bonds are issued for broader purposes like funding corporate needs, infrastructure, or government projects. |

| Risk Profile | NCDs generally offer stable returns because they are backed by assets. Secured NCDs have reduced default risk. | Bond risk varies based on issuer credit rating, market conditions, etc. Some bonds carry a higher default risk. |

| Interest Rates | NCDs typically offer higher interest rates than conventional bonds to compensate for the higher risk. | Interest rates for bonds vary depending on the issuer’s creditworthiness. Government bonds are usually safer but have lower rates. |

Although both instruments are investment vehicles in NCD vs. bonds, their distinct features—convertibility, security, purpose, risk profile, and interest rates—underscore the importance of aligning investment decisions with personal financial objectives and risk tolerance.

Also Read: Difference Between Bondholder and Shareholder: Understanding the Key Distinctions

Disconnect your funds’ static and enter the future of profits with Tap Invest. Weary of the exact old yield? Discover growth again with our cutting-edge unlisted bonds worth 18% returns. Get updated with our latest insights and today’s trends by following Tap Invest on Instagram.

When considering NCD vs. bonds or any investment, weighing the security and risk is essential. Here’s how bonds and NCDs differ regarding the level of risk they present and the security they offer.

Security and Risk

NCD vs. bonds requires security and risk profiles of bonds and NCDs. A thorough assessment of the issuer’s financial standing and credit ratings is essential in determining the risks associated with these investments.

Bonds Are Low-Risk Secured Investments

NCDs are a riskier investment than bonds, especially since bonds are frequently backed by collateral. Bonds that are guaranteed by specific assets provide investors with a certain level of security. These are known as secured bonds. Holders of secured bonds have a claim on the collateral, which can include tangible assets like real estate or intangible assets like cash reserves, in the event of default. Because of this additional security, secured bonds are a popular choice for risk-averse investors.

NCDs Are More Dangerous, Especially Unsecured Ones

NCDs, on the other hand, have a higher risk profile, mainly if they are unsecured. Debentures that lack collateral or specific assets are referred to as unsecured NCDs. As a result, investors are solely reliant on the issuer’s standing. Because they have no claim to any collateral, holders of unsecured NCDs may suffer a complete loss in the event of financial difficulty or default; this risk becomes more pronounced during economic downturns or when the issuing company faces operational challenges.

Credit Ratings for Determining Creditworthiness

Credit ratings are crucial for assessing the risk associated with bonds and NCDs in NCD vs. bonds.

Credit Rating Agencies

Organizations such as CRISIL, ICRA, and CARE provide unbiased evaluations of an issuer’s creditworthiness. A higher credit rating indicates that the issuer is more likely to repay its debts, which signifies lower risk. Conversely, lower ratings suggest a greater default risk, serving as a warning to investors. Credit ratings quantify the level of risk associated with each investment, assisting investors in making well-informed decisions.

Also Read: How to Invest in Bonds in India: Best Bonds & Simple Steps

Issuer’s Credit Rating and Debt Repayment Capability

Investors should consider several key factors before investing in bonds or NCDs.

Issuer’s Credit Rating

Always verify the credit rating assigned to the issuer by a reputable organization. This rating provides insight into the potential risk of default and reflects the issuer’s ability to meet its debt obligations.

Debt Repayment Capability

Examine the issuer’s cash flow, income statement, and balance sheet to assess financial health. Important metrics include interest coverage, debt-to-equity, and overall profitability. A solid financial standing suggests a higher capacity to repay debt, reducing the associated investment risk.

Market Situation and Industry Outlook

The broader economic landscape and the specific dynamics of a given industry can be extremely valuable. For instance, sectors experiencing downturns may pose greater risks, regardless of an issuer’s credit rating.

In NCD vs. bonds, bonds, which are frequently backed and secured by assets, are generally less risky than NCDs, which can be particularly risky when unsecured.

Investor preferences vary based on risk tolerance and financial goals. Let’s explore how these preferences influence whether bonds or NCDs better fit an individual’s portfolio.

Investor Preferences

The need for risk management and the desire for steady returns influence investor preferences for NCD vs. bonds. The decision between these two instruments ultimately depends on an investor’s investment horizon, enabling customized strategies to reach financial goals.

NCDs for Steady Returns Without Volatility in the Equity Market

NCDs are a popular choice among investors seeking steady returns free from the volatility of the equity markets.

Fixed Returns

Fixed interest payments offered by NCDs may appeal to conservative investors seeking reliable sources of income. Due to their stability, NCDs are particularly attractive during market turbulence, as stock price fluctuations have less impact on them. Investors often choose NCDs for security during uncertain economic times because their consistent returns can help insulate portfolios from stock market declines.

Fixed-Income Bonds With Varying Degrees of Risk

Although bond risk levels can differ greatly depending on the type, they also provide a consistent income stream.

A Wide Range of Options

Investors can select bonds that suit their risk tolerance, ranging from corporate bonds with varying credit ratings to government bonds, regarded as low-risk. For example, lower-rated corporate bonds may yield higher returns with greater risk, while high-grade bonds offer more security but generally have lower yields. This range allows investors to customize their bond investments based on risk tolerance and financial objectives.

Also Read: Explaining Debenture Redemption Reserve: Meaning, Application, and Necessity

Various Strategies Depending on the Investment Horizon and Risk Tolerance of the Investor

Both bonds and NCDs can accommodate a variety of investment strategies, depending on the investor’s risk tolerance and time horizon.

Risk Tolerance

Lower-rated bonds or unsecured NCDs may offer higher returns to risk-averse investors, while secured NCDs and high-grade bonds may be preferred by conservative investors seeking to minimize risk. Determining one’s personal risk tolerance is essential for choosing the appropriate instrument.

Investment Horizon

The duration of an investor’s plan may also influence their decision between bonds and NCDs. NCDs are attractive to individuals with specific short- to medium-term goals, as they frequently have fixed maturities ranging from a few years to a decade. On the other hand, investors who want consistent income over a longer time frame and wish to take advantage of compound interest might find that longer-term bonds are a good fit.

In NCD vs. bonds, bonds offer a range of options to suit varying risk levels and investment strategies. At the same time, NCDs are preferred for their consistent returns free from equity market volatility.

Leap into liquidity and use Tap Invest to make your cash work smarter. Invest without traditional constraints, free up your money, and choose flexible options that offer larger returns. Learn more about investing by watching Tap Invest’s videos on YouTube.

Comparing NCD vs. bonds is crucial for making a well-informed decision. Below is a comprehensive overview to help investors choose the best option.

Comparative Overview

An outline of the critical distinctions between NCD vs. bonds can help investors make informed decisions. Ultimately, effective portfolio management requires matching investment choices to one’s risk tolerance and financial goals.

| Feature | NCDs (Non-Convertible Debentures) | Bonds |

| Risk-Return Profile | Secured NCDs appeal to conservative investors seeking lower risk. | Bonds offer opportunities for various risk appetites, with variable rates and credit ratings. |

| Features That Favor Investment | NCDs offer fixed interest payments and appeal to risk-averse investors due to asset backing. | Bonds offer corporate, municipal, and government bonds to diversify portfolios. |

| Conservative Investors | Secured NCDs or high-grade government bonds offer capital protection and consistent income. | High-grade government bonds suit those seeking low risk and steady returns. |

| Moderate to Aggressive Investors | Unsecured NCDs or lower-rated corporate bonds provide higher yields for those accepting more risk. | Corporate bonds with lower ratings offer potential for higher returns but come with increased risk. |

| Investment Horizon | NCDs may appeal to those seeking shorter-term commitments with fixed tenures and payouts. | Bonds with fixed interest rates are ideal for investors with longer time horizons. |

Bonds with fixed interest rates that gradually lock in returns may benefit investors with longer time horizons. However, because of their fixed tenures and steady payouts, NCDs may appeal to those looking for shorter-term commitments.

Also Read: RBI Floating Rate Bond: A Secure Investment Option

In NCD vs. bonds, bonds provide investors with an excellent range of options that accommodate varying risk profiles and investment objectives. In contrast, NCDs cater to those seeking stable returns with asset backing.

Conclusion

NCD vs. Bonds are important options for people looking to invest money safely while earning some income. They both pay fixed interest, which attracts different types of investors. However, they have some differences: Non-convertible debentures (NCDs) are mainly issued by companies to meet specific funding needs and usually offer higher returns because they come with more risks. Both companies and governments can issue bonds and vary in risk and return. Some bonds are safer than others, which makes them appealing to cautious investors.

NCDs can be a good choice for those willing to take on some risk for potentially higher returns. However, before investing, it’s vital to assess the risks involved. Bonds are generally a better option for beginners or those who prefer safety because they are considered less risky.

Investors can pick from different types of bonds based on how much risk they are comfortable with, from riskier corporate bonds to safer government bonds. Bonds offer regular interest payments, providing a steady income and helping protect your money. No matter what type of investment you choose, reading all related documents, like prospectuses and credit reports, is crucial. Taking the time to understand these documents can improve your investing experience and lead to better results.Go beyond the standard and invest with Tap Invest in innovative alternative fixed-income returns. Tap Invest offers customized solutions for those seeking higher returns on the stable security of unlisted bonds. Act now to take charge of your financial future and benefit from steady income and long-term growth by diversifying your investments with Tap Invest today.